How I track daily expenses (and why it matters)

Two years of guessing, then a simple log

I started my career in mid-2022 and spent freely for two years without knowing where the money went. Since December 2024 I have logged about 90% of my expenses in Dime.

I started working in mid-2022 — new job, new city, first real salary hitting my account. For the next two years, I spent freely and genuinely could not have told you where most of it went.

I'd check my bank balance, open the credit card app, scroll through UPI, and still feel completely lost. Every app showed me a piece of the picture. None of them showed me the whole thing.

2022 to 2024

It wasn't like I was recklessly blowing money for the fun of it. I just never built the habit. Food, travel, some gadgets, nights out, subscriptions I forgot I had, random impulse buys — all of it happened, and by the time the month ended, I'd already forgotten half of it.

I'd open a statement, scroll for a bit, feel a little uneasy, and close it. That was my entire "system," if you could call it that.

By late 2024, I was done pretending that was fine. I didn't want some strict budgeting regime either. I just wanted to actually know what I was spending money on.

December 2024: I started logging

I gave myself one rule: log the expense the same day it happens.

No spreadsheet, no elaborate setup on day one. Just write it down.

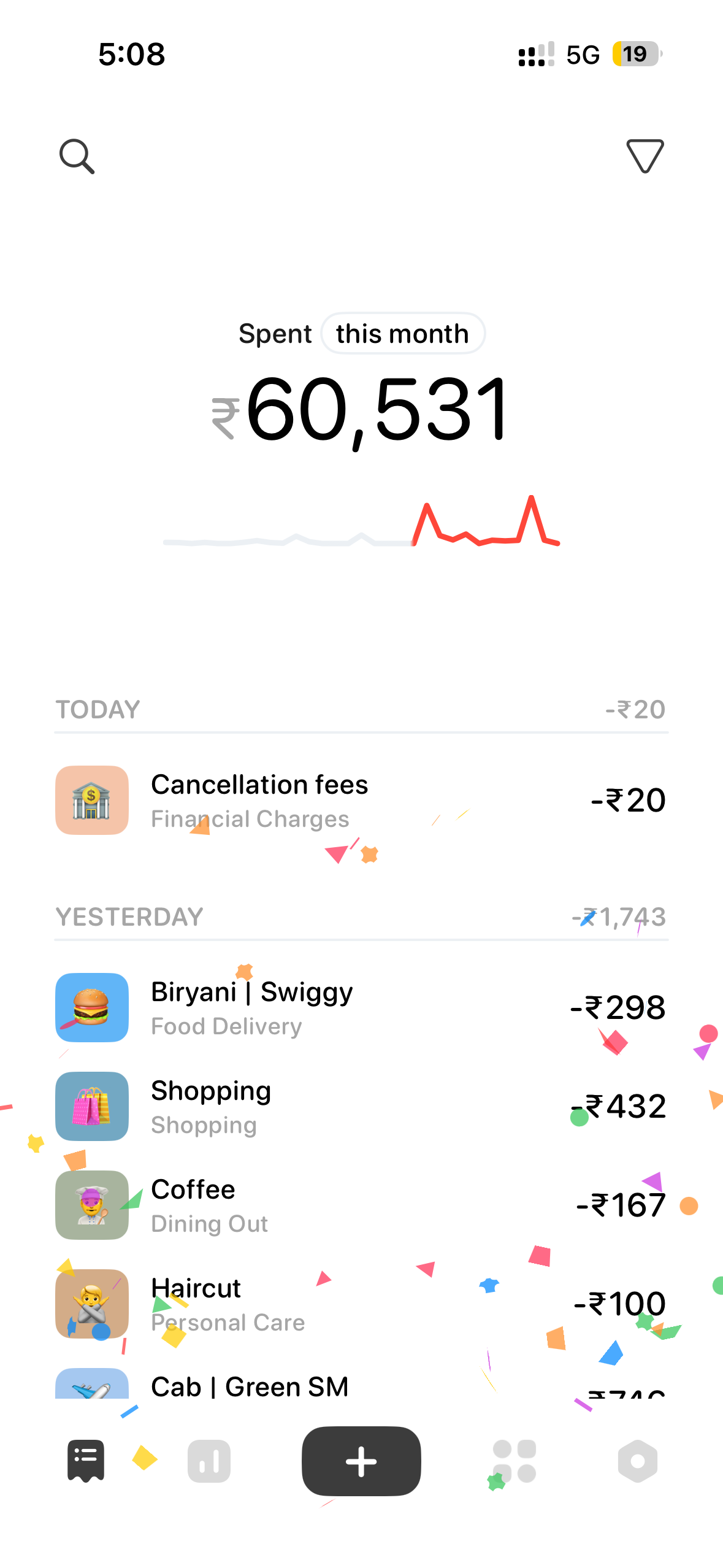

I use Dime — a free iPhone app. Open it, punch in the amount, pick a category, done. Here's what a normal day looks like in there:

Since December 2024, I've logged around 90% of what I spend in this app. The remaining 10% is usually loose cash, or something small I remember to add the next morning. Close enough for me.

Why checking my bank statement alone never worked

People tell me to "just check the bank app." That doesn't actually work for how I pay for things.

In a normal week, I might pay with a credit card, a gift card I bought earlier, UPI routed through a credit card, regular UPI straight from my bank account, or occasionally a direct bank debit. One bank statement only ever shows me a slice of the week — the rest is scattered across cards, UPI, and gift cards that never show up in any one place. Logging everything in Dime fixed that for me, because it doesn't care *how* I paid. It only cares *what* I spent the money on.

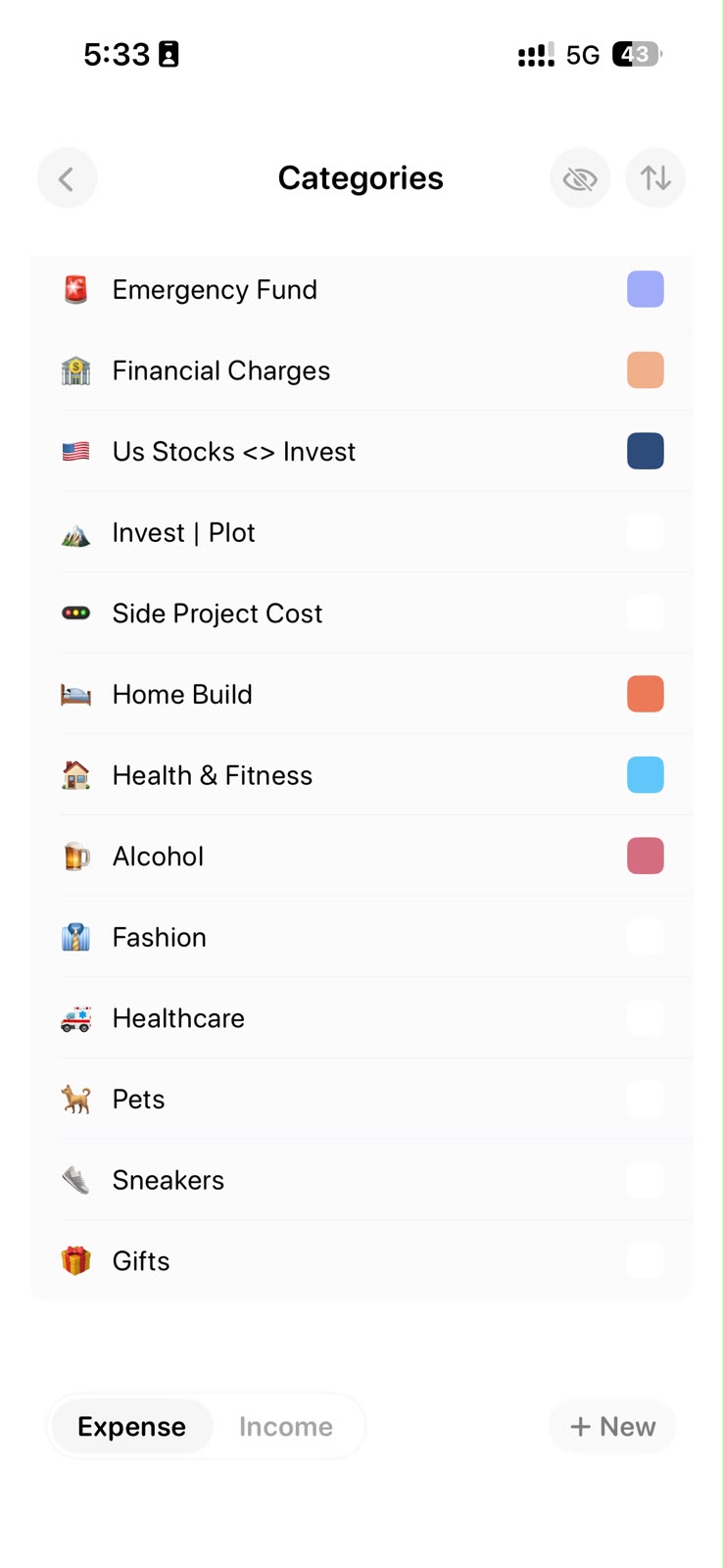

Getting the categories right

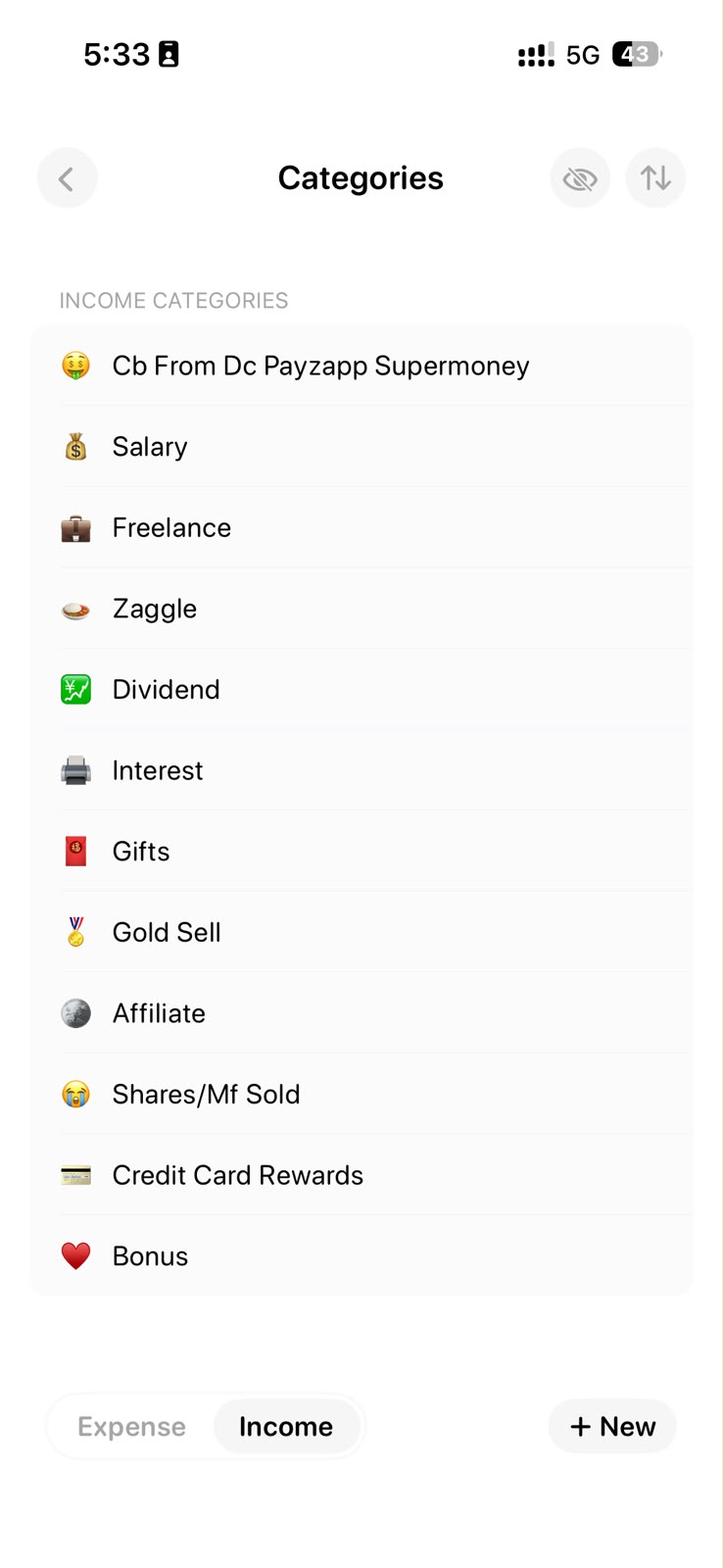

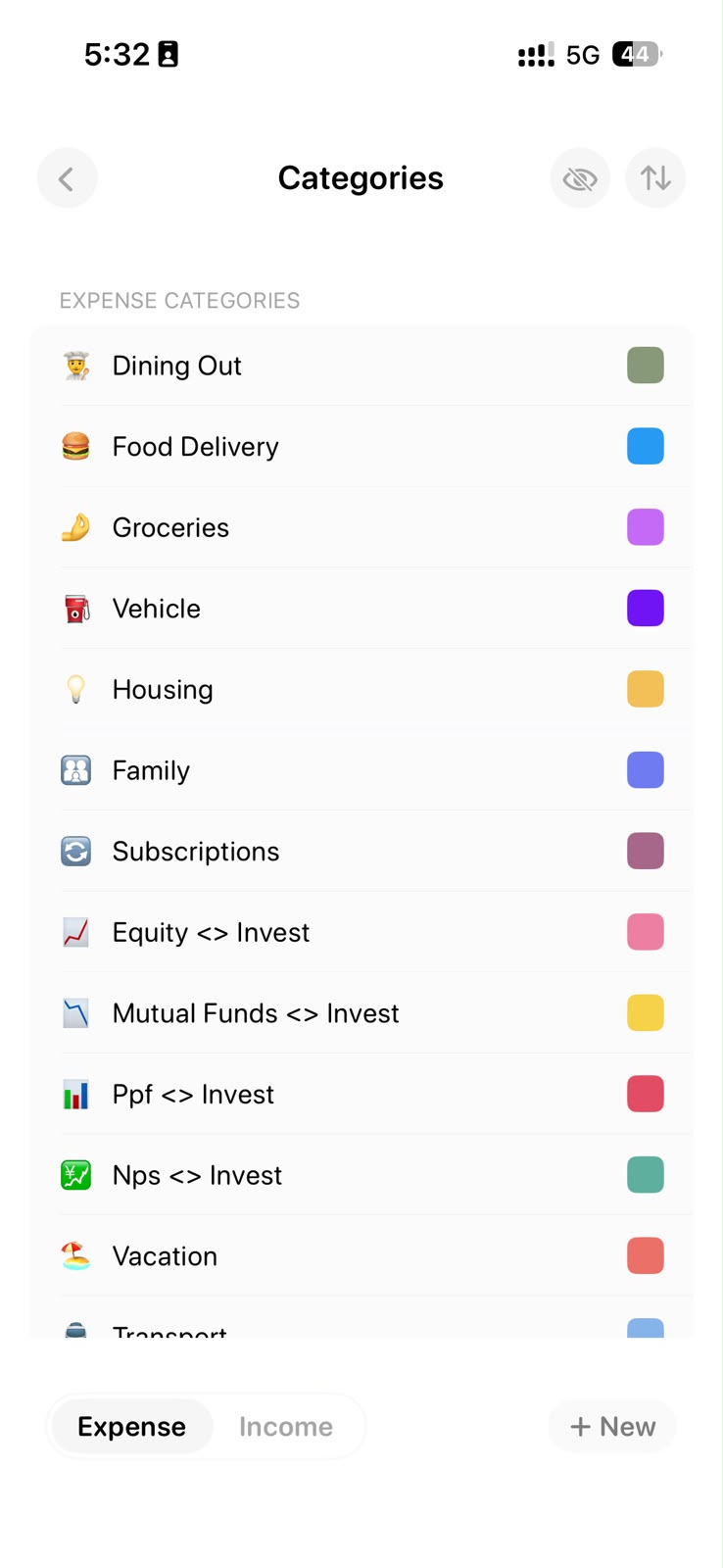

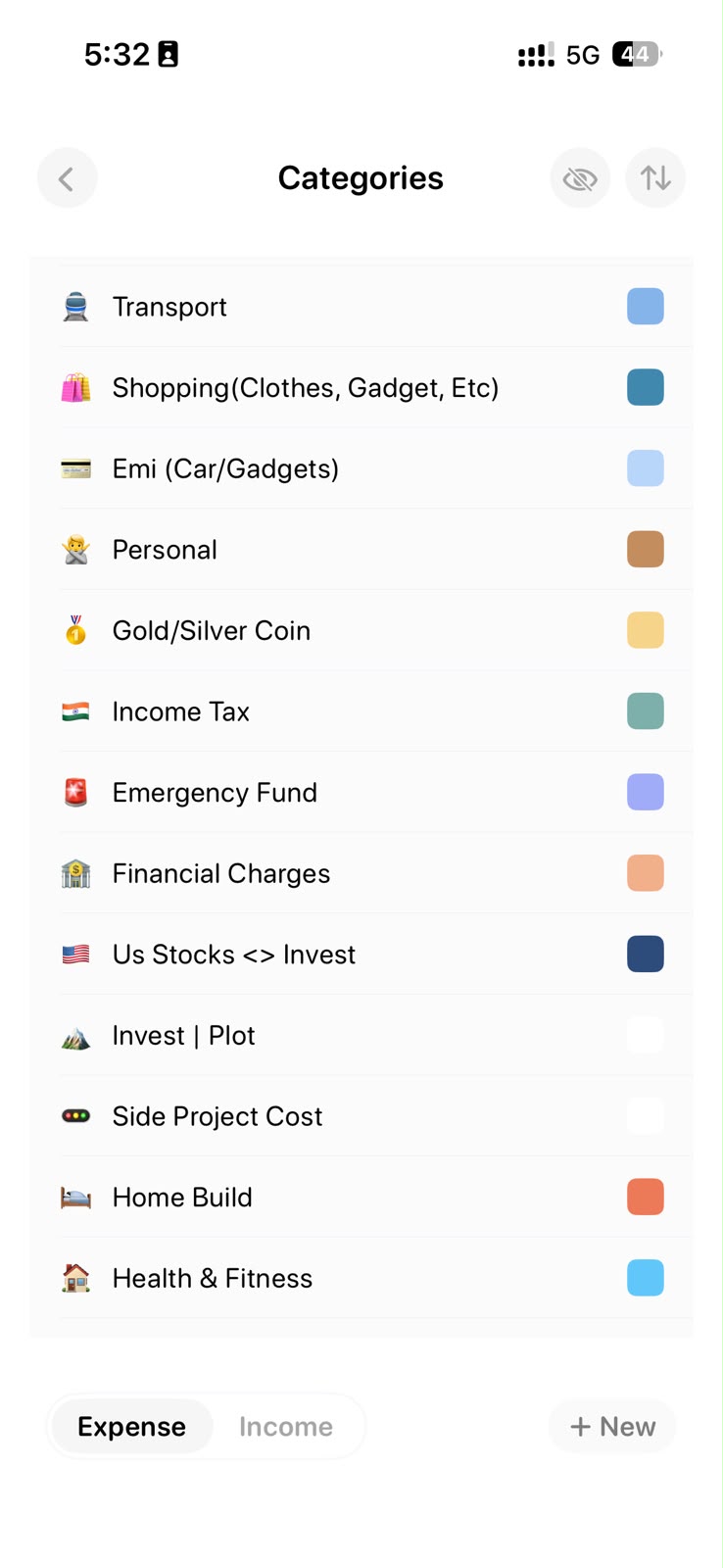

A daily log is pretty useless if everything just piles up under "misc." So I set up categories that let me later split my money into three clear buckets: income, living spend, and investments.

Income covers salary, freelance work, cashback, rewards, interest, dividends, and the occasional gift. Living spend is food, transport, housing, family, subscriptions, shopping, vacations — the ordinary stuff of life. Investments — equity, mutual funds, PPF, NPS, US stocks, a plot of land, my emergency fund — get kept firmly in their own lane so they never blur into food or shopping by accident.

Getting that naming right early is really what makes everything after this actually useful.

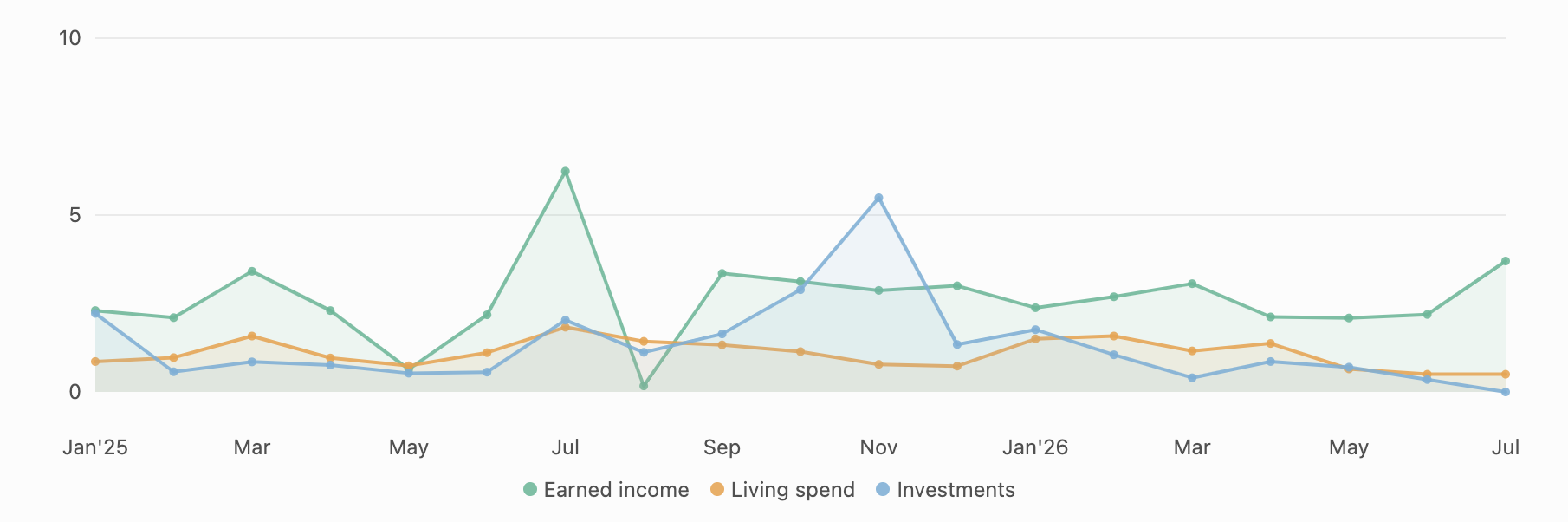

What the numbers look like now

Once income, living spend, and investments are tagged properly, I can finally see the full picture across months instead of squinting at one statement at a time:

After a few months of logging almost every day, a few things changed. I could see food, travel, and subscription spending without bouncing between three different apps. "Can I actually afford this?" got a lot easier to answer, because I already had a sense of what the week looked like. Month-end stopped ambushing me. And planning trips, using credit card rewards well, or funding a side project all got simpler.

I didn't suddenly turn frugal overnight. I just stopped guessing.

Asking questions in plain English

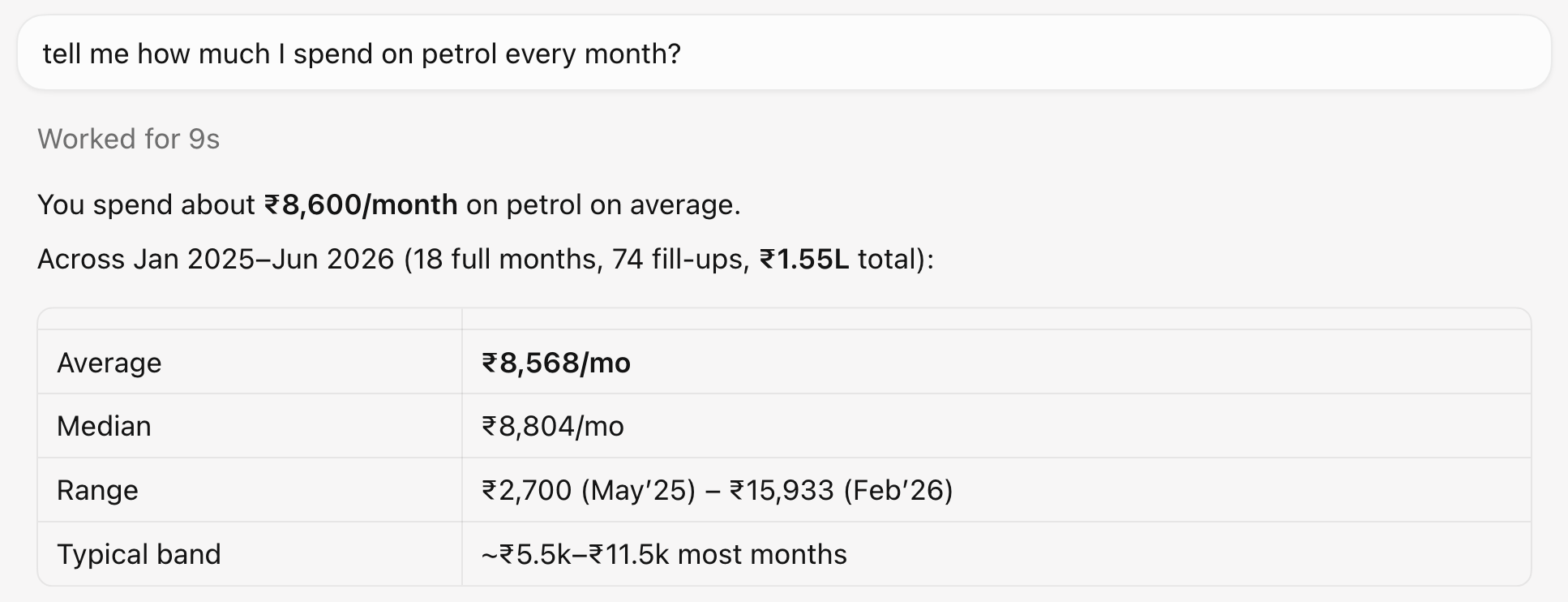

Charts tell you a lot, but sometimes I just want to ask something directly.

Dime lets me export a CSV of all my transactions. I drop that into a folder, open it up in an AI tool — I use Cursor — and just ask in normal language: how much did I spend on food last month, what were my biggest categories, has my travel spending gone up. No dashboards to build, no formulas to write. The CSV is the source, and the AI just reads it and answers.

This only works well because the categories are already clean going in. If everything's dumped under "misc," the answers come back useless. But if income, living spend, and investments are tagged properly from the start, the questions get useful almost immediately.

What I actually do, day to day

I log the expense the same day — same hour if I can manage it, but same day is the non-negotiable part. Every entry goes into the right bucket: income, living spend, or investment. Rent and fixed bills go on recurring, so I'm never relying on memory for those. I look at the whole week once, rather than obsessing over today's list. And when I want a real answer, I export the CSV and just ask in plain English.

I'm not paid to talk about Dime — I use it because it's free and simple enough that I actually stuck with it. If you're on iPhone, here's the Dime App Store link.

If you want to try this yourself

You don't need my exact categories. You need a log you'll actually keep, and category names you'll trust later.

Pick a simple tracker. Log every expense the same day for two weeks straight. On day 15, sort what you see into income, living spend, and investments, and clean up the category names if they're not working. Change one habit for the next two weeks based on whatever stood out. And if you want to go further, export a CSV and let an AI tool answer the questions you've been guessing at for years.

That's really all there is to it. I spent my first two working years guessing. Since December 2024, I've been writing it down instead. Knowing where my money actually goes has been enough.